Article: The Crisis That Closed NYSE on Wednesdays

The Crisis That Closed NYSE on Wednesdays

In the late 1960s, an unusual crisis struck Wall Street. With daily trading volume on the New York Stock Exchange soaring to new heights, the average number of shares changing hands had more than doubling in just three years. In this era before automated systems and processing, the Street soon became overwhelmed.

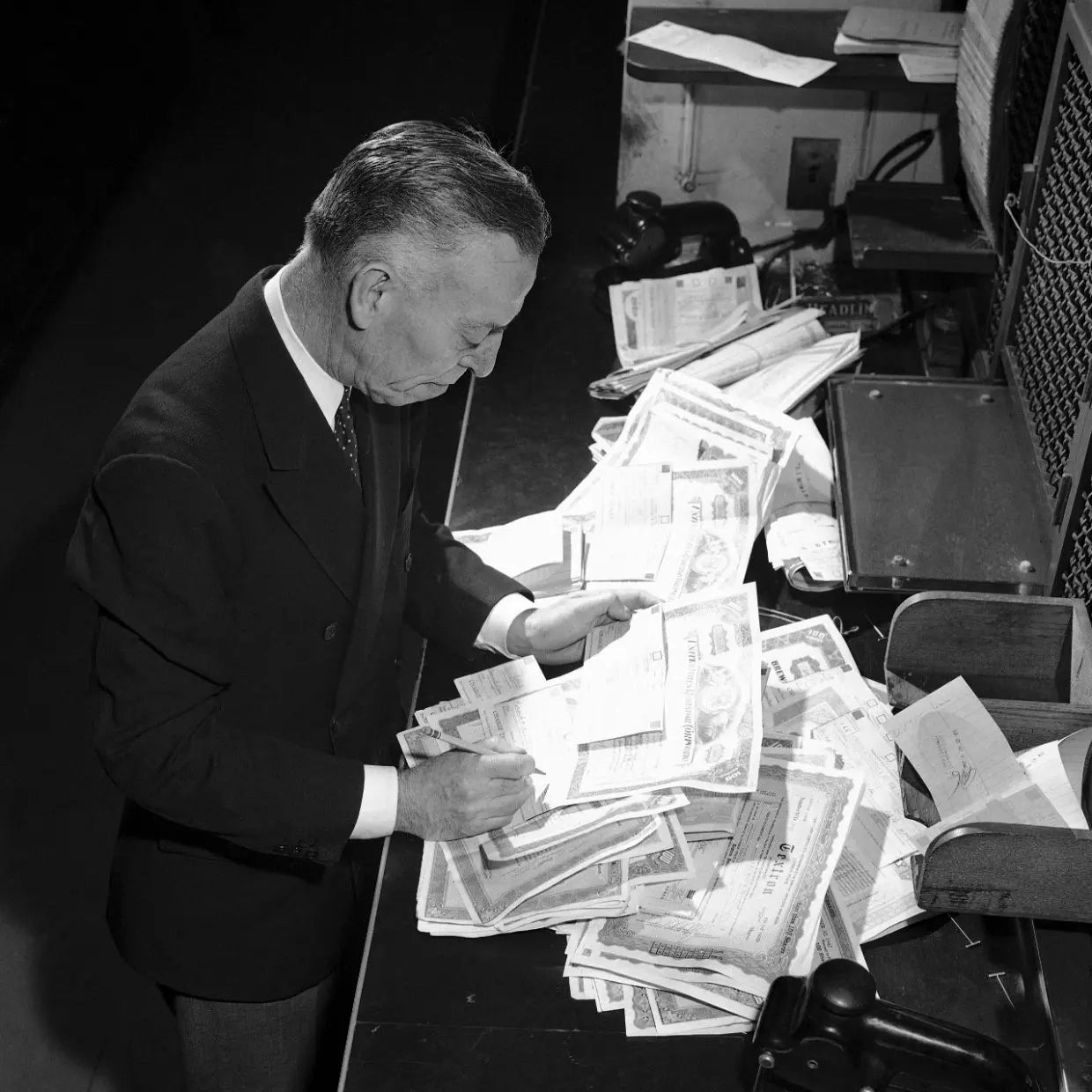

In the days before computerized trading and a centralized electronic stock delivery system, the Street depended on messengers tasked with trudging up and down Wall Street to deliver paper stock certificates by hand. By 1968, daily trading volume hit 12 million shares a day. The sheer mass of stock certificates and other paperwork overwhelmed many Wall Street back offices, the groups working behind the scenes to settle and clear trades.

What would become known as the “Paperwork Crisis” forced the NYSE to restrict trading to four days a week. For months the exchange closed on Wednesdays, and sometimes needed to close early on other days to give firms additional time to combat severe backlogs. The extra time wasn’t enough to stem the flood of “fails” — failures by firms to receive or deliver securities within five days of a trade — that rocked the street.

“A lot of firms could not separate records of fails to receive and fails to deliver,” Robert M. Gardiner, now 92, who served as managing partner of Reynolds & Co. during the crisis, recalled during a recent interview. “It became a financial problem.”

Gardiner prides himself on having run “a tight ship” at Reynolds. The firm, which was later acquired by Dean Witter & Co., was one of the few big brokerages that reported profits throughout the late ’60s. Nonetheless, the firm grappled with millions of dollars in fails.

The ongoing paperwork problems “turned the situation into a disaster…by depriving many firms of control over their records and costs,” Auburn University history professor Wyatt Wells wrote in the journal Business History Review.

Cleaner sweeping the floor of the New York Stock Exchange after closing

Cleaner sweeping the floor of the New York Stock Exchange after closing

Over just two years, about a sixth of all NYSE member firms disappeared from Wall Street, either through merger or closure, and almost every one “suffered greatly from confusion in its back office,” according to Wells.

To compound the problem, amid the chaos, thieves thrived. At a 1971 U.S. Senate hearing covered by the New York Times, U.S. Attorney General John N. Mitchell estimated that organized crime syndicates made off with more than $400 million in stolen securities.

It was a time of “painful” lessons, NYSE president Robert W. Haack wrote to NYSE members in an Exchange report released in February 1971.

While the period was traumatic for some, others embraced the frequent Exchange closures. While back office employees were hard at work, some brokerage salesmen would skip out to go work on their golf game, the New York Times reported in 1968.

Alan Epstein, who spent more than half a century as a broker, said paperwork problems didn’t bother him in the least. In the late ’60s, he worked for Josephthal & Co., another brokerage firm that weathered the crisis and could even afford perks like providing free turkeys to employees on Thanksgiving.

“It was a well-run firm,” Epstein, now 88, said of the firm since acquired by Oppenheimer & Co. “If there were backroom problems, I wasn’t aware of them. I was only aware that we closed early and the brokers got bonuses.”

Still, others like Reynolds’ Gardiner were painfully aware of the mess, and couldn’t wait to put it behind them. “The most important thing is that once the crisis was recognized, the industry took care of correcting it,” Gardiner said. The automation of trades through computers — spearheaded by Haack and considered to be one of his crowning achievements — provided much-needed relief from the paperwork logjam. But automation didn’t come cheap and smaller firms couldn’t afford it at all, according to Wells. The firms that did pursue automation, however, had a strong incentive to increase transactions and pursue new lines of business. “Computers cost the same when busy or idle, so the more transactions a firm processed, the lower its cost per transaction,” Wells wrote.

Later, the creation of a central recordkeeping institution, the Depository Trust Corporation (DTC), added another layer of protection and efficiency.

Today, the DTC and high-tech trading allow for trade volumes that are exponentially greater than those that birthed the Paperwork Crisis. Trading volume on the NYSE is typically north of 900 million shares a day, and often exceeds one billion shares. In 1968, then a record-breaking year for the Exchange, the average daily volume didn’t quite hit 13 million shares.

The stark contrast between now and then isn’t lost on Gardiner. “Can you imagine what it would look like today if they only did 13 million shares a day?” he said. “They do that at the opening bell now.”

{kind=link}